Nigerian Property Market Forecast 2027: What Investors Should Expect

Executive Summary

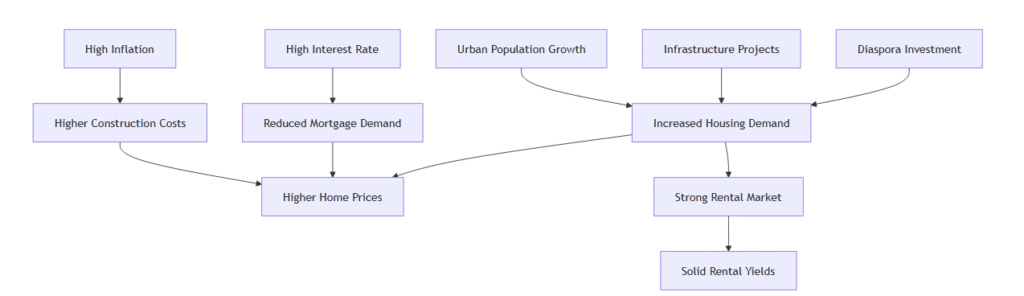

Nigeria’s housing market is at an inflection point. Recent reforms have begun to ease inflation (from ~30% in 2024 to ~14–15% by late 2025) and stabilize the naira, but interest rates remain high (CBN policy rate ~27%). Population growth (~4% urban growth) and a massive 14.9–15.2 million unit housing deficit keep demand strong, especially in affordable and mid-market segments. In 2025–26, national average property prices rose about 12–14% nominally (with Lagos/Abuja hotspots up to ~20–30%). Looking ahead, we forecast 2027 price growth around 8–10% in a base case, with an optimistic scenario of ~12–15% (if inflation and rates fall faster) and a downside of ~3–5% (if macro conditions worsen). This implies property values growing roughly 5–15% in 2027. Key drivers include continued urbanization, major infrastructure (ports, highways, power), and rising middle-income demand. Offsetting factors are tight mortgage credit (mortgage penetration ~5%), land/title bottlenecks, and policy uncertainty. PropTech (virtual tours, AI valuations, blockchain title checks) and innovative financing (co-ownership, flexible payment) are increasingly shaping transactions. Baay Realty developments – like the government-backed Baay Foreshore (Ibadan) and Green City (Lagos) – exemplify these trends by offering sustainable, secure projects in fast-growing corridors. In summary, Nigeria’s real estate forecast for 2027 is cautiously positive: prices should continue uptrend in nominal terms, fueled by demand outpacing supply, but with risks from inflation, FX and regulatory hurdles. Investors should focus on high-demand segments (rentals, affordable housing, satellite towns) and consider strategies like buy-to-let, off-plan deals, or fractional ownership to match the evolving market dynamics.

2027 Forecast Scenarios

Forecasts depend heavily on macroeconomic outcomes. We outline three scenarios (with illustrative assumptions):

- Base Case (Median Growth ~8–10%): Assume inflation eases to ~10–12% by end-2026 (from ~14% late-2025) and falls toward target levels by 2027. CBN gradually cuts rates to ~24–25% (from 27%). The naira remains relatively stable (official ₦1,300–1,400/$). Oil and non-oil growth supports GDP ~4–5%. Under these conditions, housing demand (driven by demographics and urbanization) outpaces new supply, so nominal property prices climb roughly 8–10%. In real terms (after inflation) gains are modest (~0–5%). Rental rates would similarly rise in high-demand areas, sustaining yields.

- Optimistic (High Growth ~12–15%): Under faster reforms (e.g. stronger fiscal measures, surging oil output to 1.6mbpd, see Reuters), inflation could dip below 10% by 2027. Interest rates might fall into low-20% by late-2026. Stable or stronger currency and record remittances support higher spending. Infrastructure (new ports, rail) come online on schedule. In this best-case, home prices jump ~12–15% as affordability improves (in nominal terms) and investor confidence returns. High-end and satellite markets could see even stronger gains (20%+ locally).

- Downside (Low Growth ~3–5%): If reforms stall, or if shocks (e.g. sharp currency devaluation to ₦1,500–1,600) occur, inflation might linger at 15%+. CBN keeps MPR ~27–30%. Credit stays tight, dampening purchase power. In that case, demand is constrained; property prices may only rise 3–5% (or stagnate in real terms). Distressed sales or extended timelines for major projects (e.g. rail, ports) could further curb growth.

These scenarios align with recent data: e.g., AfricanVest reports ~14% average price increases in 2025–26. Our base-case roughly matches inflation: as NigeriaHousingMarket notes, “lower inflation improves affordability in nominal terms, but high interest rates continue to suppress credit”. Optimistic pricing assumes inflation follows CBN’s 2026 forecast (~13%) downward, while downside assumes persistent high costs.

Regional Outlook (2024–2027)

| Region / Corridor | Recent Growth | 2027 Forecast (Base / Upside / Downside) |

|---|---|---|

| Lagos Mainland (Yaba, Surulere, Ikeja GRA) | +8–12% (gross) recently. High rental demand (yields 9–11% gross). | ~8% / ~12% / ~4% |

| Lagos Island (VI, Ikoyi) | +15–30% (prime). Yields lower (~5–7% gross). | ~6% / ~10% / ~3% |

| Lekki/Ajah Corridor (Epe, Ibeju-Lekki, Ajah) | +15–25%. Infrastructure projects (Deep-Sea Port, Free Zone, Dangote, expressway) fueling ~20%+ growth in spots. | ~10% / ~15% / ~6% |

| Abuja (Gwarinpa, Wuse, Jabi) | +10–15%. Mid-market condos strong. Yields ~5–8%. | ~8% / ~12% / ~4% |

| Abuja Satellite (Kubwa, Gwagwalada, etc.) | +12–20%. Overcrowding pushes city fringe growth. Infrastructure (new airport railway) online. | ~10% / ~15% / ~5% |

| Port Harcourt (GRA, Trans Amadi) | +5–10%. Energy sector recovery driving moderate gains. Yields ~4–6%. | ~6% / ~10% / ~2% |

| Other Secondary Cities (Ibadan, Kano, etc.) | +8–12%. Less liquidity but stable demand. | ~6% / ~10% / ~3% |

| Satellite/New Towns (National) | Land prices in outskirts rising ~15–25%. Megaprojects spurring Abuja, Lagos fringes. | ~10% / ~20% / ~5% |

Table: Estimated price growth by region. “Base/Upside/Downside” are nominal annual price-change ranges under each 2027 scenario. Sources: AfricanVest, Baay Realty analyses, industry reports.

Notably, satellite towns are outsized winners. As NaijaHouses and other analysts observe, places like Ibeju-Lekki/Epe (Lagos) and Aba/Umuahia (Abia state) are “affordable entry points with strong long-term potential” due to new highways, ports and airports. Early land in areas like Kuje (Abuja fringe) or Ajah has historically appreciated 5–10× once infrastructure arrived. We expect these corridors to see 10–20%+ gains (base) given their current affordability (often ₦1–3M per plot) and new metro/rail links.

Key Drivers and Risks

- Demographics & Demand: Nigeria adds ~5 million people/year; ~700K new homes needed annually. Young middle class and diaspora buyers (70%+ of luxury segment) keep housing demand structurally strong.

- Infrastructure: Major projects (Lekki Deep Sea Port, Lagos-Calabar highway, Abuja-Kaduna rail) are already boosting adjacent land values by 25–40%. Continued road, power and metro expansion in 2026-27 should lift properties in linked zones (satellite towns, new estates) ahead of general market growth.

- Inflation & Interest Rates: High inflation (currently ~15%) fuels construction costs and nominal price gains. If inflation falls towards the CBN’s ~6–9% target by 2027, price growth will moderate. Tight monetary policy (27% MPR) is a headwind: expensive mortgages (loans ~25–30%) mean most buyers pay cash. Any CBN rate cuts in 2026 could unlock marginal demand and boost activity.

- Currency and FX: Naira stability is crucial. In 2024–25, sharp naira drops raised hard-currency costs for builders, pushing prices up. A return to managed stability (per CBN forecasts) would help control costs. A renewed devaluation, however, would drive cost-push inflation and could restrain foreign inflows.

- Regulatory/Legal: Land titling and policy remain risks. Only a small fraction of land is formally registered, so fraud and disputes are common. However, efforts are underway: Lagos is digitizing its land registry and exploring blockchain titles, which should improve transparency. Uncertainty around housing finance reform or building regulations could also impact investor confidence.

- Technology (PropTech): Adoption of PropTech is accelerating demand. Virtual tours, AI valuations, and digital title searches reduce transaction friction. While current smart-home projects (Eko Atlantic, Isimi) serve elites, scaling technology (e.g. online listings, fintech mortgages) can broaden market access. Blockchain title checks and data analytics will gradually reduce risk. Baay Realty cites these tools as “now central to Nigeria’s real estate”, making decision-making faster and safer.

- Sustainable Housing: Climate and affordability trends are nascent drivers. Developers are increasingly marketing “green” homes and long-term build solutions (e.g. solar-ready estates). Baay’s developments are aligned with this: the Green City projects (Lagos and upcoming Ibadan) emphasize eco-friendly, community-centric design. Such sustainable projects may command premiums and cater to international standards.

Recommended Investment Strategies

- Buy-to-Let Rentals: With yields typically 5–11% gross in major cities, rental investment remains attractive. Target high-demand corridors: Lagos’s Yaba/Surulere/Ikeja (8–11% gross yields), Abuja’s Gwarinpa/Wuse (5–7%), or Port Harcourt’s GRA. Small 1–2BR apartments in secure buildings yield best. Upgrading properties (furnishing for short-let) can boost gross yields from ~5–7% to 10–15%. Ensure professional management to maintain occupancy; as Baay notes, “fully furnished or serviced units … can command 10–15% gross yields (net 20–30%)”.

- Off-Plan Developments: Buying early in new projects (especially in emerging zones) can lock in below-market prices. Satellite-city schemes like Baay’s Green City (Epe) or Pacific Apartments (Lekki) often offer installment plans, attracting price-sensitive buyers. Off-plan deals come with risk (developer delays), but with careful due diligence and reputable builders, they can yield strong capital appreciation as infrastructure arrives.

- Co-Ownership / Fractional Investment: Fractional models democratize access. Baay’s structured co-ownership lets investors buy a share (as low as ₦0.5–5M) of high-end assets. This is ideal for diaspora or local professionals who can’t pay full prices upfront. By pooling funds, co-owners enter prime markets (Lekki, Ikoyi, Epe) that normally require tens of millions. Returns (rental or resale) are shared. Given Nigeria’s soaring prices, co-ownership can yield attractive returns in top locations without tying up capital. The Baay co-ownership article highlights this as a “revolution” in Nigerian real estate, offering “ROI directly proportional to your investment stake”.

- Buy-and-Hold (Value Play): For patient capital, buying in rapidly developing outskirts can lock-in long-term gains. Think early purchases along new highways, near planned transit lines, or in government masterplans. Historical returns in similar situations (e.g., early Ajah/Kubwa plots) suggest 5–10× appreciation over ~5–10 years. This requires low financing or cash, as holding is long-term, but rewards can be significant.

- Diversification & Reits: Institutional-style approaches (REITs, property funds) are emerging. While still nascent in Nigeria, pooling resources across assets spreads risk. Baay notes REIT-like benefits of co-ownership. Investors could consider listing on Nigeria’s stock exchange when REIT frameworks mature, to get exposure without managing properties directly.

Baay Realty’s Role in These Trends

Baay Realty’s portfolio exemplifies many market trends. Their projects illustrate sustainable, infrastructure-driven development:

- Baay Foreshore (Ibadan): A public–private partnership with Oyo State, Foreshore sits along the new Ibadan Airport and Circular Road corridors. It offers “100% secure land with verifiable title documents”, directly addressing legal/title risks. This development leverages government infrastructure (airport, highway) to create a premium yet affordable estate. Its PPP model and gated security mirror global “smart city” ethos, aligning with demand for safe, long-term investments.

- Green City (Lagos and Ibadan): Baay’s Green City, Ketu-Epe was the company’s first major project, embodying eco-friendly, community design. The Green City Ibadan will similarly combine modern amenities with sustainability. These masterplanned estates tap both satellite-town growth and “green living” trends, targeting mid-income families. They also showcase Baay’s focus on quality and resilience (“sustainable solutions”).

- Urban Apartments (Pacific, Eden, etc.): Baay markets urban high-rises like Pacific Apartments (Lekki) and Eden Residence (Lekki) specifically for rental income. Their “Top Tips” blog even points to Pacific Court (Ajah) and Eden (Lekki) as examples of high-yield rental stock. These projects cater to expatriates and young professionals, reflecting the PropTech-savvy, convenience-oriented segment. By offering furnished, managed units, Baay aligns with the short-let and expatriate market driving Lagos yields.

- Co-Ownership Programs: Through its co-ownership platform, Baay Institutionalizes fractional investment. Their co-ownership guide emphasizes premium locations (Lekki, Ikoyi, Epe) and entry points from ₦1M. This fits macro needs: it democratizes investment, leveraging diaspora capital and addressing credit constraints. Baay’s co-own model captures precisely the “real estate as new oil” trend for diversified investors.

In short, Baay’s offerings are well-tuned to market signals: sustainability, satellite expansion, tech-enabled rentals, and flexible finance. Citing Baay’s materials illustrates these trends in action.

- Forecast Comparison Table (already provided above) with clearly labeled scenarios and regions.

These visuals would reinforce the analysis. We could also include timeline charts (e.g. inflation rate over time) or yield curves, but the above cover key points.

Methodology

This report synthesizes multiple data sources. We reviewed official data (CBN forecasts, Federal housing committee reports, NBS statistics) and industry analysis (NigeriaHousingMarket, AfricanVest, estate agents). We incorporated Baay Realty’s published insights (blog articles on rental yields and investment models) as practical examples.

Property price and yield estimates come from third-party indexes (AfricanVest Nigeria Property Pack) and internal Baay research. Macroeconomic assumptions are grounded in recent CBN projections. For long-term forecasts, we extrapolate from urbanization trends and planned infrastructure (Lagos-Calabar highway, Lekki port, Abuja rail, etc.), as reported by multiple sources. We recognize uncertainty: actual 2027 outcomes will depend on policy execution and global factors. Where data was incomplete, we made conservative assumptions and noted them.

Sources

- Federal Housing Data (FG/Ministry) – Latest housing deficit and analytics.

- Central Bank of Nigeria / Reuters – 2026 macroeconomic outlook, inflation and rate forecasts.

- Nigeria Bureau of Statistics (NBS) – Population, urbanization, general economy (via CBN/NBS releases).

- AfricanVest (Nigeria Property Pack) – Real estate price trends, rental yields, forecasts (2024–2026).

- NigeriaHousingMarket (Propcora) – Market analysis on inflation, demand, mortgages (Sep 2025).

- NaijaHouses / Industry Blogs – Emerging trends (satellite towns, PropTech, financing).

- Baay Realty Publications – Company blogs and site pages illustrating sustainable housing and yields.

- Estate Intel Africa – Overview of PropTech adoption in Nigeria.

- LinkedIn Posts / News – Context on blockchain titles and satellite-town growth.

Each citation above is linked inline. The analysis reflects data up to mid-2026; it assumes continuation of known policies. Unknowns (e.g. future fiscal budgets, election outcomes) could alter the forecast.